Understanding how your advisor is compensated is key to knowing what you’ll pay and what incentives they have. It’s important to know how much an advisor will cost before hiring them.

Financial advisors and financial planners can charge for their services in a variety of ways. Some advisors charge clients directly via fees, for example, a percentage of assets managed or an hourly rate. Others earn commissions from financial products they sell, meaning the client isn’t billed upfront but indirectly pays through product costs. In many cases, advisors use a combination of fees and commissions. This guide breaks down the common compensation models: commission-based, fee-only, fee-based, and hourly/flat-fee planners. We’ll explain how each structure works, how much they typically cost, and the pros and cons of each approach.

Industry Overview: The trend in recent years has been a shift away from pure commissions toward fee-based arrangements. By 2025, ~three-quarters of advisors’ revenue comes from direct client fees, while only about 23% comes from commissions. A decade earlier, many advisors relied on commissions, but evolving regulations and client preferences have driven a move to transparent fee models. Most investors today prefer to pay an advisor a straightforward fee rather than commissions. In one survey, 61% of households favored fee-based pricing, versus 39% who preferred commissions. With that context in mind, let’s examine each compensation style in detail.

Commission-Based Financial Advisors

What it means

A commission-based advisor earns income from commissions on products they sell or transactions they facilitate. Typically, the mutual fund company, insurance carrier, or brokerage pays the advisor for selling their products. Those commissions are usually embedded in the product’s cost. For example, if a commission-based advisor sells you a mutual fund with a 5% front-end load, 5% of your investment might go to the advisor’s firm as a commission. Many commission-based advisors are essentially brokers or insurance agents by role. These advisors often advertise “free” financial advice because you don’t write them a check. Instead, they get paid by the product providers. There is debate and potential regulation changes in the work around who can call themselves a financial advisor.

How they charge

Commissions come in several forms: upfront sales charges (loads) on mutual funds, commissions on insurance policy premiums, or transaction fees/markups on stock and bond trades. Typical commission rates might range from around 3% to 6% of the investment amount for many financial products. For instance, a life insurance agent could earn a large percentage of your first-year premium as commission. A broker might get a fee for trades or a “trailer commission” from mutual funds (often around 0.25% annually via 12b-1 fees). Commission-based advisors at brokerage firms may also have incentive structures like sales targets or bonuses. Advisors employed by a bank might receive a base salary with bonuses tied to how many products they sell. These are other forms of indirect compensation that the client doesn’t see billed, but which can influence the advisor’s recommendations.

Pros of hiring a commision based advisor

Commission-based compensation has some potential advantages for certain clients:

No Direct Out-of-Pocket Fee. You typically do not pay the advisor a fee upfront. The advice may appear “free” since the advisor is paid by product providers. This can be appealing if you’re averse to writing a check for advice. The costs are embedded in the products you buy.

Suitable for One-Time Needs. If you only need a one-time transaction (eg. insurance policy or load fund) and don’t anticipate ongoing advice, a commission model can be cost-effective. You pay once through the product purchase rather than an ongoing fee.

Access to a Wide Range of Products. Commission-based advisors (including insurance agents and brokers) often can offer a broad set of financial products because that’s how they earn their living. This one-stop access can be convenient if you are looking for product solutions and implementation.

May Work for Smaller Portfolios. For investors with very small portfolios, paying a 1% annual fee might be impractical. A commission-based advisor might be willing to work with clients with modest assets since they get paid per transaction instead. If you hold a suitable investment for a long time, a one-time commission could cost less than continuous fees.

Cons of hiring a commission based advisor

There are important drawbacks and risks with commission-based advisors:

Potential Conflicts of Interest. The biggest concern is that commission-based advisors have incentives to sell or trade products. Their recommendations might be influenced by the commission payout.

Suitability Standard (Not Fiduciary). Commission-based advisors are generally held to a “suitability” standard rather than a fiduciary standard. This means their recommendations just have to be suitable for your needs, not necessarily the very best or lowest-cost option. They aren’t legally obligated to put your interests first, and may not have to disclose all conflicts of interest. In contrast, fee-only advisors typically act as fiduciaries (more on that later).

Less Transparent Costs: With commissions, the costs to you are often hidden or hard to see. You won’t receive a bill from the advisor, but you are paying via fees (higher expense ratios or insurance premiums). This lack of transparency can make it difficult to evaluate what you’re truly paying for advice.

Incentive for Unnecessary Trading or Products. In a worst-case scenario, commission-compensated brokers might engage in churning: excessive trading just to generate commissions.

Long-Term Costs and Limitations. You might think you’re avoiding fees, but over the long term you could end up paying more.

Bottom line

Commission-based advisors make money without directly charging you. This can seem attractive, but you are likely indirectly paying through product fees and potentially higher costs. This model can work for product-centric needs or for clients who truly only need occasional transactional help. However, be aware of the conflicts of interest. Always ask what commissions an advisor might receive and ensure any product recommended truly suits your situation. If you prefer more transparent, ongoing fiduciary advice, you may lean toward fee-only or hybrid models instead.

Fee-Only Financial Advisors

What it means

A fee-only financial advisor is compensated solely and directly by the fees their clients pay. In practical terms, “fee-only” means the advisor’s only revenue comes from you (the client). These fees may be a percentage of assets under management (AUM), flat planning fees, hourly fees, or subscriptions. They do not earn money from fund companies, insurance carriers, or any third-party for selling you something. Because of this, fee-only advisors typically operate as fiduciaries, legally obligated to put your interests first and minimize conflicts.

How they charge: Fee-only advisors can use a variety of fee structures:

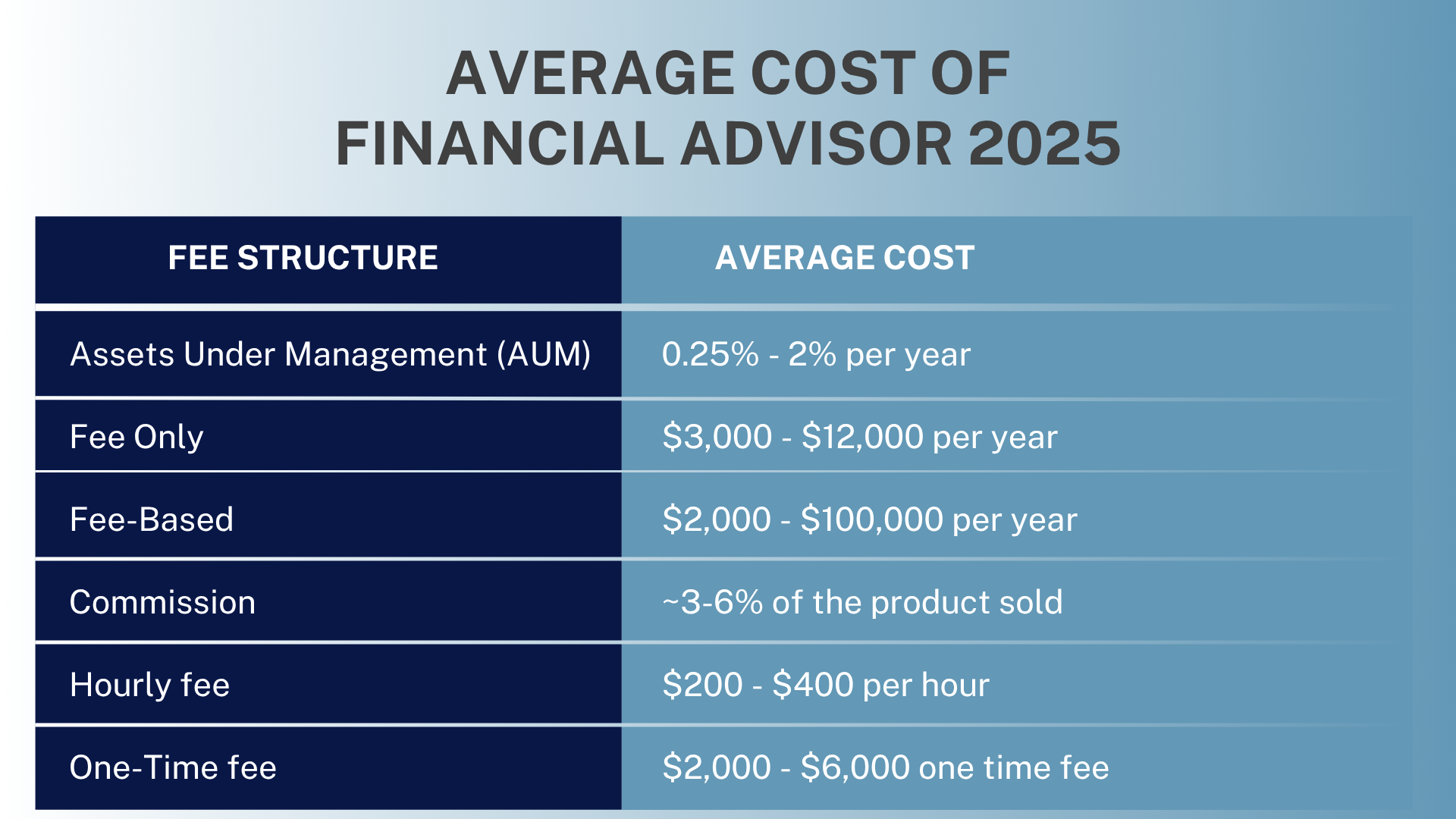

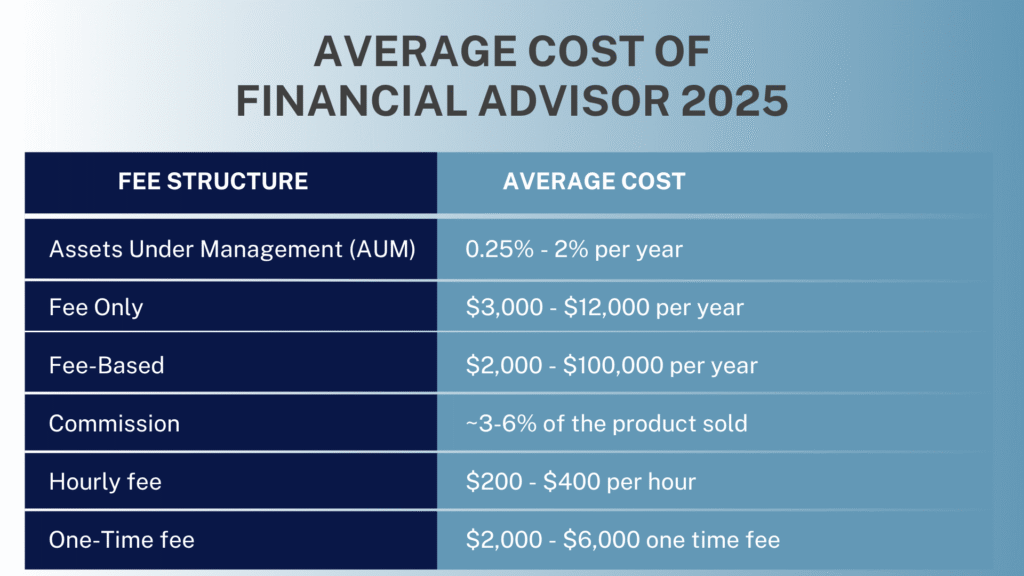

Assets Under Management (AUM) Percentage: This is one of the most common structures. The advisor charges a set annual percentage of your assets, usually around 1% per year. For example, if you have a $500,000 portfolio, a 1% AUM fee equals $5,000 per year. Many firms use tiered rates (e.g. 1% on the first $1M, 0.75% on the next $4M, etc.), so the percentage may drop for larger asset values. The fee is often deducted quarterly from your account.

Hourly Fees: Some fee-only planners charge an hourly rate for consultations or ongoing advice, instead of a percentage of assets. Typical hourly rates range roughly from $200 to $400 per hour. Hourly billing is usually for as-needed advice or specific projects. We will discuss pros and cons of hourly planners in a dedicated section below (“Hourly and Flat-Fee Planners”).

Flat or Project-Based Fees: A fee-only advisor might offer a flat fee for a specific service or financial plan. For example, a comprehensive financial plan might cost a one-time flat fee of $1,000–$3,000, depending on complexity. This could cover an analysis of your situation and written recommendations. Some advisors also offer one-time consultations or second-opinion services for a set fee.

Subscription Fees. Increasingly, some fee-only advisors use a subscription model. Meaning the charge a fixed monthly or annual fee to cover an ongoing advisory relationship. This could be a monthly subscription (e.g. $100–$300 per month) or an annual retainer (often in the $2,000–$7,500 per year range). High-complexity or high-net-worth cases could be higher. Retainer fees are not tied to assets; instead, they’re based on the scope of services. This model is popular among advisors serving younger professionals or those without large portfolios.

No matter the structure, because fee-only advisors only get paid by you, their incentives are aligned with providing advice and services that justify the fee. There’s no financial reward for recommending a high-commission product. However, the costs are explicit, you will see the fee being charged, whether via invoice or account deduction.

Pros of hiring a fee-only advisor

Working with a fee-only advisor offers several key benefits:

Fiduciary, Client-First Advice: Fee-only advisors must put your interests first and generally adhere to the fiduciary standard. Since they never earn commission you don’t have to worry that a policy or fund is being pushed on you for compensation. This can give you peace of mind about the objectivity of the advice. You’re paying them to give the best guidance possible, much like you would pay an attorney or accountant.

Transparent Costs: The cost of advice is usually very clear and transparent with fee-only arrangements. You agree on the fee structure upfront (be it 1% of assets, $X hourly, or a flat dollar amount), and you can see exactly what you’re paying on statements. There are no surprise charges buried in product fine print.

Aligned Incentives for Portfolio Growth. If you pay a percentage-of-assets fee, your advisor’s compensation rises and falls with your portfolio’s value. This can align their motivation with yours. It gives them an incentive to help grow your assets over time (and avoid big losses), since that grows their fee as well.

Holistic Planning and Service. Because fee-only advisors charge for advice and ongoing management, they often provide more comprehensive financial planning beyond just investments. Many will help with retirement planning, tax strategies, estate planning basics, budgeting, etc., as part of their service. Fee-only advisors are generally “advice-centric” rather than “product-centric,” which can mean a broader, holistic approach to your finances.

Cons of hiring a commission based advisor

Fee-only arrangements also have some downsides to consider:

Out-of-Pocket Cost to the Client. The most obvious con is you will pay the advisor directly, and it can be expensive in dollar terms, especially as your assets grow. A common fee of ~1% annually might sound small, but it adds up. On a $1,000,000 portfolio, 1% is $10,000 per year. Over many years, that can compound and eat into your investment returns. For smaller portfolios, some advisors charge a higher percentage.

Perceived “High” Cost vs. Commission Model. Fee-only advisors are often perceived as more expensive than commission based, because the cost is transparent. A commission-based product might cost you as much or more in the long run, but psychologically, writing a check or seeing a fee deducted can be more painful. Some investors, especially those not used to paying for financial advice, may feel the fees are steep. Sticker shock can be a barrier, even if the advice is worth it.

Minimum Asset Requirements. Many fee-only advisors, particularly those using the AUM model, set minimum account sizes (often $250,000, $500,000 or even $1 million) to ensure the relationship is profitable for them. This means smaller investors or those just starting out might have difficulty finding a fee-only advisor willing to take them on.

Bottom line

Fee-only financial advisors offer independent advice with no product-sales bias, which can greatly benefit consumers seeking unbiased, fiduciary guidance. You have clear visibility into what you’re paying. However, you need to be comfortable paying that fee and ensure the services provided are worth the cost. If you have substantial assets or need ongoing planning, a fee-only arrangement can pay off. For those with limited assets or who only need occasional help, a full-time fee-only AUM relationship might be too expensive. Hourly or project-based planners or robo-advisors might be good alternatives.

Fee-Based Financial Advisors

What it means

The term “fee-based” (often confused with fee-only) usually refers to a hybrid compensation model. Fee-based advisors do charge client fees (like an AUM percentage), but can also earn commissions. In other words, they blend the two approaches. Many advisors at larger brokerage firms or insurance companies fall into this category. They may be dually registered as both investment advisor representatives (able to charge fees) and broker/agents (able to earn commissions).

It’s important to note that “fee-based” is not the same as fee-only. Fee-based advisors can receive third-party commissions, whereas fee-only do not. Always clarify this when you see the term. Typically, a fee-based advisor will disclose in their agreements that in addition to client fees, they “may receive commissions or incentives from product sales.”

How they charge

Fee-based advisors have a standard fee (AUM fee or flat fee) plus the ability to collect commissions on products. Common scenarios include:

Charging an AUM fee for investment management, and if they recommend an annuity or insurance policy, they earn a commission.

Charging a financial planning fee, and if you implement investment or insurance products through them, they also get commissions.

Some fee-based advisors might reduce their fee if they receive commissions, or vice versa, but this varies. Ideally, they provide full disclosure so you know all sources of their compensation.

Pros of hiring a fee-based advisor

The fee-based model has some advantages, essentially combining elements of the prior two models:

Access to a Wide Range of Products and Services. Because fee-based advisors can earn commissions, they are often licensed to sell insurance, annuities, or loaded funds – things a pure fee-only advisor might not offer directly. This means as a client, you have one advisor who can both craft a financial plan and implement product solutions. For instance, if part of your plan calls for life insurance or an annuity, a fee-based advisor can execute that in-house. This one-stop convenience and broader toolset can be a plus.

Ongoing Advice with Transaction Capability. You get the benefit of ongoing advisory support (for the fees you pay), along with the ability to handle transactions. In market downturns, for example, a fee-based advisor paid via AUM can provide guidance without worrying about making a sale. They can also take care of transactional needs when they arise. Essentially, you have a relationship (via the fee component) rather than purely one-off sales. Many fee-based advisors pride themselves on offering holistic financial planning.

Potentially Lower Explicit Fees. Some fee-based advisors offset their fee with commissions earned. For example, an advisor might charge a lower AUM fee (say 0.5% instead of 1%) if they know they will get commissions from products. In theory, this could reduce the direct fee you pay.

Can Serve Different Client Preferences. Fee-based advisors can adapt to client needs – for a client who hates commissions, they can operate almost like fee-only; for a client who doesn’t want to pay much upfront, they can lean on commissions. This flexibility can make advice accessible to a broader range of clients.

Cons of hiring a fee-based advisor

Along with the benefits, the fee-based approach carries some of the same concerns as commission models, plus added complexity:

Conflicts of Interest Still Exist. Even though a portion of the fee-based advisor’s income comes from client fees, the possibility of commission influence remains.

Less Transparent Fee Structure: Fee-based arrangements can be more confusing to understand. You might be paying an advisory fee and indirectly paying via product commissions. It may not be immediately clear how much you’re paying in total.

Possibility of Bias Toward In-House Products. If the advisor works for a firm that has its own financial products (like a brokerage or insurance company), they might have incentives or quotas to sell those, even under a fee-based model. For example, some firms give advisors a bonus for hitting certain commission benchmarks or using certain funds.

Bottom line

Fee-based advisors can offer a blend of comprehensive advice and product implementation, which can be convenient. If you go this route, ensure you work with someone you trust who will be transparent about what they’re earning on both sides. Many fee-based advisors do operate ethically and put clients first; they use commissions only as needed. In fact, the industry movement toward fee-based models is partly to deliver more holistic, long-term planning while reducing overt product-pushing. Just remember that “fee-based” doesn’t remove all conflicts. An honest advisor will explain how they get paid in each scenario.

Hourly ad Flat-Fee Planners (Pay-As-You-Go)

Not everyone needs or wants an ongoing financial advisory relationship charging a percentage of assets. For those who prefer to pay only for the advice they need, when they need it, the solution is often an hourly or flat-fee financial planner. These advisors are typically fee-only (no commissions at all). Their fee structure is worth breaking out separately because it’s distinct from the traditional AUM mode and growingl. Hourly and flat-fee planners offer a consumer-friendly, a la carte approach. For example you might pay for a few hours of advice or a one-time project, rather than committing to an annual fee.

How they charge

Hourly Rate. Hourly rates for financial planners usually range from about $150 to $400 per hour, with a median around the mid-$200s. The exact rate often depends on the planner’s experience, location, and credentials. You and the advisor would agree on the scope of work and an estimate of hours. Some advisors charge different rates for different services or have junior staff bill at lower rates. If you only need a couple of hours of advice you might pay a few hundred dollars total. This model is analogous to how you might hire an attorney or CPA by the hour.

Flat or Project Fees. Instead of billing every hour, some planners offer flat-fee packages. Common examples: a one-time financial plan for a set price (e.g. $2,000 for a comprehensive plan covering all aspects of your finances), or a retirement analysis for $1,000, a college funding plan for $500, etc. The advisor will define what’s included. According to industry data, a full financial plan typically costs around $1,000 to $3,000. Of course, prices can vary with complexity, a high-net-worth, complex situation might be $5,000+, whereas a straightforward plan for a younger individual could be under $1,000. The key is that it’s a fixed quote for the project, regardless of hours.

Whether hourly or flat, these planners do not earn commissions, they are paid solely by the client’s fees, like other fee-only advisors. The difference is the fees are decoupled from assets. You pay for the advisor’s time and expertise directly.

Pros of Hourly/Flat-Fee Advisors:

Pay Only for What You Need. The biggest advantage is cost control and efficiency. You can engage the advisor for a specific issue or a limited time, and you’re only paying for that service. If you have a decent handle on some aspects of your finances and just need help with a particular area you don’t have to sign over a percentage of all your assets or pay an ongoing retainer you might not fully use. This a la carte approach can be very cost-effective for people with less complex needs or DIY inclination, you get professional advice when needed and handle the rest yourself.

Accessible to Clients with Low Assets. Because hourly/flat-fee advisors don’t require managing a portfolio, they generally have no minimum asset requirements. They are willing to work with young professionals, those just starting out, or people who primarily need advice on budgeting, debt, or financial planning rather than investment management.

No Ongoing Commitment: You can essentially “try before you buy” – get some advice and then decide if you need more. There’s no long-term contract locking you in (beyond perhaps a small engagement letter for a project).

Fiduciary, Unbiased Advice. Like other fee-only advisors, hourly/flat-fee planners are typically fiduciaries and do not have product sales influencing their advice. You can expect objective recommendations. Many hourly planners explicitly position themselves as consumer advocates who want to offer conflict-free advice by charging only for time.

Budget-Friendly & Predictable. Knowing the cost upfront (or having a good estimate) helps you budget for financial advice. If an advisor says a financial plan will be $2,500, you can decide if that fits your budget. Similarly, if you pay $250 for an hour and get the answers you need, that might be a small investment for potentially large financial improvements. Compared to giving up 1% of your assets every year, many find a flat fee approach more palatable.

Cons of Hourly/Flat-Fee Advisors

No Continuous Monitoring or Proactive Management. With project-based or hourly advice, once the engagement is over, the onus is typically on you to implement and maintain the plan.

Costs Can Add Up for Extensive Needs. While you avoid an open-ended 1% fee, if you end up needing a lot of hours, the costs might approach what an AUM fee would have been.

Variable Quality and Scope. Not all hourly or flat-fee planners offer the same depth of service. Some might only do narrow project scopes and won’t delve beyond what you’ve paid for. There’s a risk that an advisor limits the time to the budget rather than what might be truly needed to solve your problems.

Paying Upfront for Potential Value Later. With an AUM advisor, the fee comes out of your investments gradually, and if your portfolio grows, it somewhat “pays for itself.” With hourly or flat fees, you typically pay out-of-pocket (often upfront or as you go). This can sting, especially if you’re paying a large lump sum for a plan.

Bottom line

Hourly and flat-fee financial planners can be a fantastic option for those seeking targeted advice or a comprehensive plan without committing to ongoing fees. They shine for clients who are comfortable implementing advice on their own or who have specific questions to be answered.

Choosing the Right Model for You

There is no one-size-fits-all answer to which compensation model is best. Each has its place, and the “right” choice depends on your personal financial situation, your comfort with fees, and the complexity of services you need. When evaluating the cost of a financial advisor, keep these general guidelines in mind:

Always ask “How do you get paid?” before engaging an advisor. A trustworthy advisor will clearly explain their fee structure and any potential outside compensation. Don’t be shy, knowing this upfront is crucial. You have a right to know if they earn commissions, charge hourly, have asset-based fees, or any combination thereof. Transparency builds trust.

Understand what you’re getting for the cost. For example, a 1% AUM fee may include comprehensive wealth management, investment selection, rebalancing, ongoing planning updates, etc. An hourly engagement may be narrower in scope. A commission-based “free” service might only focus on selling a product. Compare not just the dollars, but the services and value provided. Sometimes paying a fee is worth it if you receive high-quality, tailored advice (studies show clients often stick with fee-based relationships due to the value they perceive).

Consider your own preferences and behavior. If you know you’d never call an advisor who charges by the hour (for fear of running up a bill), maybe an AUM or retainer model is better so you feel free to reach out anytime. If you absolutely hate the idea of paying commissions and wondering about conflicts, lean toward fee-only. If you have significant assets and want continuous oversight, an asset-based fee could be reasonable. If you’re just starting out or have a one-time decision, an hourly consult might suffice. The good news is you can shop around, most advisors offer an initial meeting at low or no cost to discuss how they work and what it would cost you.

Beware of “free” advice – you may be paying indirectly. As we’ve discussed, advisors who don’t charge you upfront are making money somehow, often through commissions or quotas. That doesn’t inherently make them bad, but you need to be aware of how those costs will ultimately come out of your pocket (through product expenses or suboptimal choices). There’s no completely free lunch. If an advisor’s services seem free, do a bit more digging.

Look for credentials and reviews. Regardless of how an advisor charges, ensure they have reputable qualifications (such as CFP®, CFA, etc.), a clean regulatory record and transparent reviews from current or former clients. You can find all three using Valinor’s Find an Advisor Tool. Fee-only advisors often highlight their fiduciary oath. Commission-based advisors can still be ethical and helpful, especially for specific needs, but you want someone who puts clients first, not sales. You can have good and bad actors in every model, so vetting the individual or firm is important.

Key Takeaway

The cost of hiring a financial advisor can range from a few hundred dollars for a consultation to tens of thousands per year in asset-based fees or commissions. What you should focus on as a consumer is value for cost. A good advisor, regardless of how they charge, should ideally save or earn you more money in the long run than they cost. These savings could come through better investment performance, avoidance of mistakes, proper insurance coverage, tax savings, or simply greater peace of mind and time saved. When that value proposition makes sense, paying for advice is well worth it.

On the flip side, if an advisor’s cost is eating away at your returns or their incentives don’t align with your goals, it may be time to re-evaluate the relationship or seek a different compensation arrangement. The encouraging news is that the industry is evolving: more advisors are offering flexible fee structures (hourly, flat, subscription) to meet clients’ needs, and commission-heavy models are less dominant than in the past. As a consumer, you have more choice than ever. Use this guide as a starting point to weigh the pros and cons of each approach.

Finally, don’t let cost alone deter you from getting advice if you need it. Some people avoid seeing a financial planner because they fear it’s too expensive, only to make costly mistakes that far exceed an advisor’s fee. There are affordable options out there, including those who charge by the hour or offer scaled-down services. The important thing is to find a trustworthy advisor whose pricing model you understand and are comfortable with. When you do, the cost of advice becomes an investment in your financial future, rather than an expense.